All Categories

Featured

Table of Contents

Adolescent insurance coverage provides a minimum of defense and can supply insurance coverage, which might not be offered at a later day. Quantities provided under such insurance coverage are generally minimal based upon the age of the youngster. The present limitations for minors under the age of 14.5 would certainly be the greater of $50,000 or 50% of the amount of life insurance coverage effective upon the life of the candidate.

Juvenile insurance coverage might be marketed with a payor advantage cyclist, which offers waiving future premiums on the child's plan in case of the fatality of the person that pays the costs. Elderly life insurance coverage, often referred to as graded death benefit plans, provides qualified older applicants with minimal entire life protection without a clinical evaluation.

The allowable problem ages for this type of coverage range from ages 50 75. The maximum problem quantity of coverage is $25,000. These plans are generally a lot more expensive than a totally underwritten plan if the individual qualifies as a typical risk. This sort of coverage is for a little face quantity, usually bought to pay the burial costs of the guaranteed.

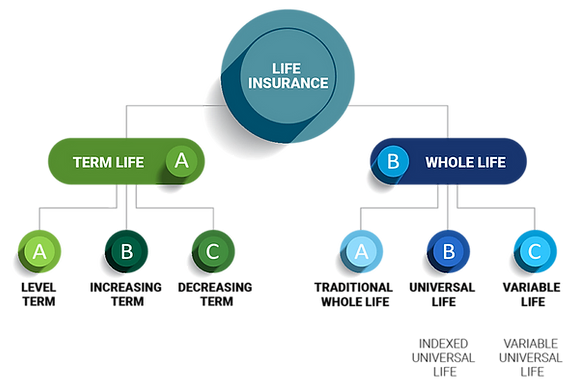

Our term life alternatives consist of 10, 15, 20, 25, 30, 35, and 40-year plans. The most popular type is level term, suggesting your payment (premium) and payout (death advantage) stays level, or the same, till completion of the term period. This is the most straightforward of life insurance policy options and calls for really little maintenance for plan proprietors.

Who are the cheapest Best Value Level Term Life Insurance providers?

For instance, you might offer 50% to your spouse and split the remainder among your adult youngsters, a parent, a close friend, or perhaps a charity. * In some circumstances the survivor benefit might not be tax-free, learn when life insurance policy is taxed

1Term life insurance coverage supplies temporary defense for an important duration of time and is typically more economical than irreversible life insurance policy. 2Term conversion guidelines and restrictions, such as timing, may apply; for example, there may be a ten-year conversion benefit for some items and a five-year conversion privilege for others.

3Rider Insured's Paid-Up Insurance policy Acquisition Choice in New York. There is a price to exercise this rider. Not all getting involved policy owners are eligible for dividends.

Compare Level Term Life Insurance

We may be compensated if you click this advertisement. Ad Level term life insurance policy is a policy that supplies the exact same survivor benefit at any type of point in the term. Whether you die on the very same day you take out a plan or the last, your beneficiaries will receive the exact same payout.

Plans can likewise last until defined ages, which in many situations are 65. Beyond this surface-level info, having a greater understanding of what these strategies require will aid ensure you purchase a policy that satisfies your requirements.

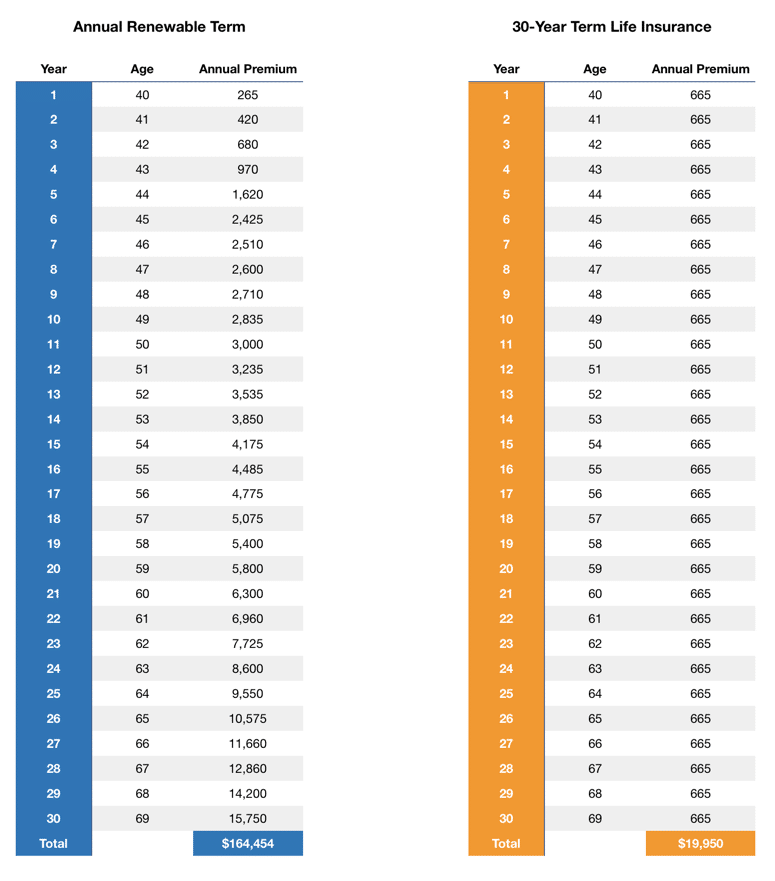

Be mindful that the term you choose will affect the costs you pay for the plan. A 10-year level term life insurance policy plan will set you back less than a 30-year plan because there's much less opportunity of a case while the strategy is energetic. Reduced threat for the insurance firm relates to reduce premiums for the policyholder.

How does Level Premium Term Life Insurance work?

Your household's age need to also affect your policy term option. If you have young children, a longer term makes good sense since it protects them for a longer time. If your kids are near their adult years and will be financially independent in the near future, a much shorter term might be a much better fit for you than an extensive one.

When comparing whole life insurance coverage vs. term life insurance, it deserves keeping in mind that the latter normally expenses less than the former. The result is extra coverage with lower premiums, supplying the very best of both worlds if you need a considerable quantity of protection however can't pay for an extra pricey plan.

What does a basic Level Term Life Insurance Rates plan include?

A degree survivor benefit for a term plan typically pays out as a round figure. When that takes place, your successors will obtain the whole quantity in a single payment, which amount is not thought about income by the internal revenue service. Those life insurance coverage earnings aren't taxed. Level term life insurance. Some degree term life insurance coverage business permit fixed-period payments.

Interest settlements received from life insurance coverage policies are considered earnings and are subject to taxes. When your level term life policy expires, a couple of various points can happen.

The disadvantage is that your renewable level term life insurance will certainly come with higher premiums after its initial expiration. We may be made up if you click this ad.

Level Term Life Insurance Benefits

Life insurance policy business have a formula for determining danger making use of mortality and passion. Insurance firms have countless clients securing term life policies at the same time and use the costs from its energetic plans to pay surviving recipients of various other plans. These firms use mortality to estimate the amount of individuals within a specific group will certainly file fatality cases annually, which info is made use of to determine average life span for possible policyholders.

In addition, insurer can invest the cash they obtain from costs and boost their earnings. Since a level term plan doesn't have cash value, as an insurance holder, you can not spend these funds and they do not offer retired life revenue for you as they can with entire life insurance policy plans. Nonetheless, the insurance provider can spend the cash and make returns.

The adhering to section details the advantages and disadvantages of level term life insurance policy. Predictable costs and life insurance policy coverage Streamlined plan framework Potential for conversion to irreversible life insurance Minimal insurance coverage duration No money worth buildup Life insurance premiums can enhance after the term You'll discover clear benefits when comparing level term life insurance to various other insurance coverage kinds.

What are the top Level Term Life Insurance Policy providers in my area?

You constantly understand what to anticipate with inexpensive degree term life insurance policy protection. From the moment you take out a policy, your premiums will never ever alter, assisting you prepare monetarily. Your insurance coverage will not vary either, making these policies effective for estate planning. If you value predictability of your settlements and the payouts your successors will certainly get, this kind of insurance might be an excellent fit for you.

If you go this route, your costs will boost however it's always great to have some adaptability if you desire to keep an energetic life insurance policy plan. Renewable degree term life insurance policy is an additional choice worth thinking about. These policies permit you to maintain your current strategy after expiry, giving versatility in the future.

{kind=link}

Latest Posts

Family Funeral Policy

Aarp Funeral Insurance

Life Insurance Instant Quote Online Dallas